2025 to be a year of recovery for Sydney offices

A recovery in the nation’s battered office property market will begin in Sydney this year as rents rise for space in the best addresses and the cycle of falling asset values bottoms out, according to top fund managers.

However, the Melbourne CBD market is expected to remain in the doldrums for at least another year before the falling valuations of the city’s office towers finally level out.

The prospect of interest rate cuts later this year, combined with improving demand for space is critical to the more sanguine outlook for Sydney at local property fund manager Investa and US giant PGIM.

Investa’s research head David Cannington and managing director of PGIM Real Estate Peter Hayes expect 2025 to be a year of recovery at least in pockets of the Sydney CBD. For high-quality office buildings in the most sought-after location, the city’s business core, they expect values to stabilise and more buildings to change hands.

That improved sentiment follows a two-year downward cycle where some assets have lost as much as 30 per cent in value as interest rates and bond yields jumped while demand for space faltered in the switch to flexible workplaces.

Investa’s Mr Cannington said headwinds for the sector from the post-COVID work transition were easing as hybrid patterns become more settled.

As well, lower inflation and anticipated interest rate cuts would ease pressure on business conditions, factors that would spur leasing demand and support capital growth. That, in turn, would make offices block more attractive investments in 2025, he said.

A key factor in valuing commercial real estate is the capitalisation rate, or cap rate, an industry standard that is similar to an investment yield. As cap rates rise, values usually fall, unless offset by rental growth.

Cap rates for prime Sydney office towers rose to just over 6 per cent last year from about 4.4 per cent in early 2022 when office tower values are considered to have peaked.

“We expect [cap rates for] Sydney CBD prime market assets have largely ‘topped out’ and will see moderate compression through 2025, while Melbourne CBD prime assets are likely to see at least another 12 months before cap rates start to compress,” Mr Cannington said.

But not all office markets were expected to recover this year. While cap rates for top Sydney office blocks have levelled off – signalling an end to falling valuations – there are more declines to go in other CBDs, including Melbourne’s, according to Mr Cannington.

There are signs that investors are becoming more comfortable too, after a slew of office transactions last year in Sydney CBD’s financial core district that provide evidence of cap rates – and thereby values – stabilising. Higher grade offices at 388 George Street, 5 Martin Place and 333 George Street among others sold for prices that represented capitalisation rates of between 6 per cent and 6.5 per cent.

By the end of 2024, more than $4 billion worth of offices in Sydney’s financial core had changed hands, a tally that is greater than the previous four years combined.

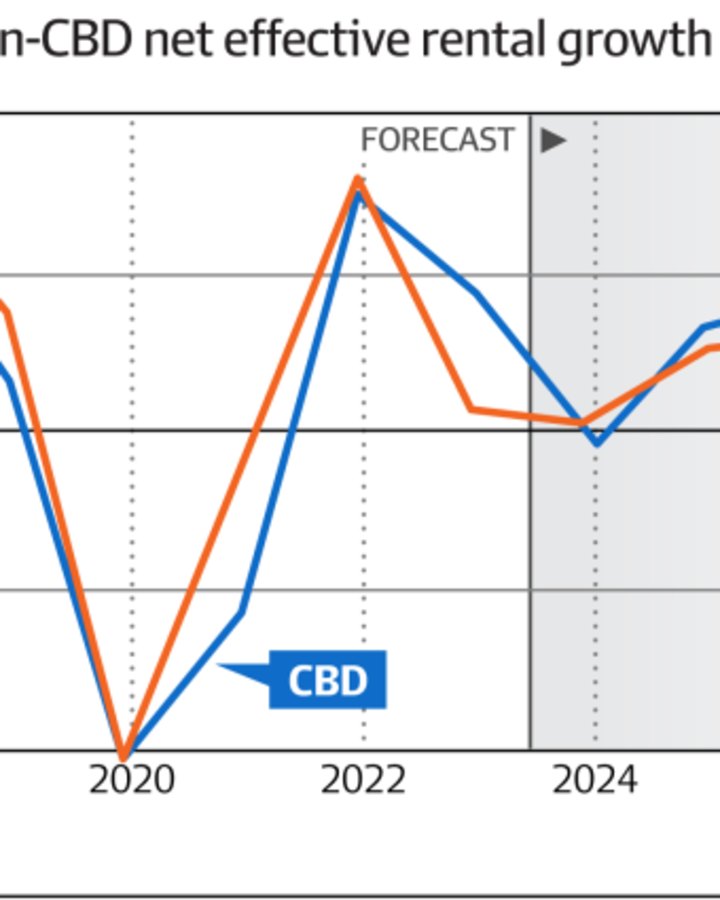

PGIM Real Estate’s Mr Hayes said CBD office assets in some markets such as Sydney – alongside Seoul, Singapore and Tokyo – were expected to outperform their non-CBD counterparts, notching up rental growth due to the limited supply of prime office space.

“An improving regional outlook is set against country-by-country differences, but in most markets values have corrected and we are at the start of a recovery that rewards early movers across all investment styles,” Mr Hayes said.

“Forecasters typically underpredict the strength of rental growth recoveries. The likelihood is the same will happen in 2025 where you would see rental growth for offices, excluding China, beat expectations.”

According to Macquarie analysts, investment demand for higher quality offices would increase this year amid expectations of rising rents and the belief that the worst of the COVID-19 volatility had passed.

“Despite broader challenges for the sector, pre-leasing activity is lifting with occupiers committing to new or refurbished offices well ahead of completion amid strong competition for high-quality space,” Macquarie said in its 2025 office outlook note.

“For investors, office pricing appears to have fallen well below replacement costs, and higher cap rates are creating good entry points for new investment.”

Macquarie expects new property fund vintages to emerge in 2025 as value-add investors look to bag strong returns made possible by buying at the bottom of the office cycle.

Rising stress levels would create opportunities for investors to acquire new buildings and sites at discounted prices from developers struggling with refinancing risks, high construction costs, and lower sales prices, it said.