$3.5b of offshore dry powder looking for shopping centre deals

The pool of foreign capital eyeing Australian retail assets has doubled from last year to more than an estimated $3.5 billion, pointing to a pick-up in deal volumes this year as investors return to the increasingly positive sector.

A flurry of transactions just before Christmas spurred foreign interest in the sector and while the majority of the capital demand was domestic, offshore participation was increasing, JLL’s senior director of retail investments Nick Willis said.

“We are currently monitoring over $3.5 billion of offshore core and core plus mandates looking to allocate to the sector, significantly up on prior years,” Mr Willis said.

In December alone, Melbourne-based fund manager Fawkner Property acquired Cairns Central for $390 million and Settlement City for $102.4 million, investor Haben bought Stockland Townsville for $238.5 million across two deals, and Vicinity divested Dianella Plaza for $76.25 million.

Momentum has continued into the new year with property platform ISPT understood to have entered into due diligence talks to sell Eastgate Bondi Junction in Sydney.

The 15,000-square-metre shopping centre has Coles, Aldi, Kmart and Dan Murphy’s as anchor tenants.

Since October, ISPT has been looking to pivot away from shopping centres as it considers whether to merge with infrastructure powerhouse IFM Investors. This led to the property platform putting up for sale a $600 million portfolio of five assets, which included Eastgate Bondi Junction, from its core fund.

JLL’s Mr Willis and Simon Hatcher, and Stonebridge’s Carl Molony, Philip Gartland and Justin Dowers, are managing the Eastgate Bondi Junction sale campaign. Both agencies declined to comment.

Retail tops table

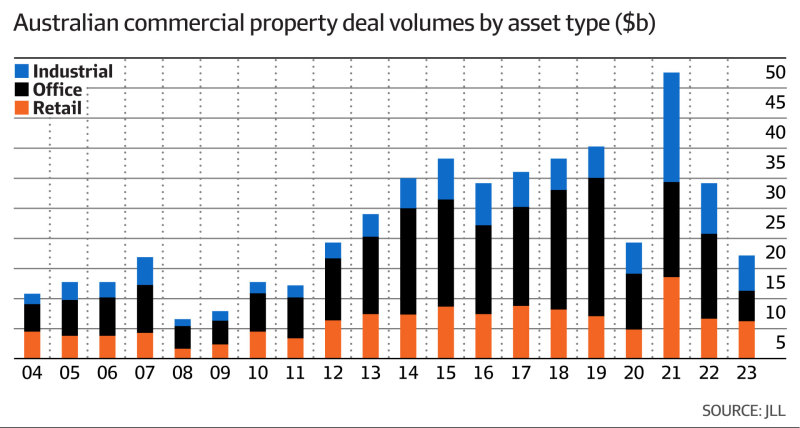

The slew of shopping centre deals at the end of last year culminated in retail being the most traded type of commercial property asset in 2023, the first time that has happened in 20 years.

In calendar year 2023, there were $6.12 billion worth of retail asset sales, which accounted for 36 per cent of traditional commercial property asset sales. About 60 per cent of those sales, in dollar terms, were transacted in the final quarter.

Sentiment around the sector is improving. JPMorgan analyst Richard Jones last week said the outlook for large malls was positive as population growth would offset an expected decline in per-capital discretionary spending.

By comparison, office transactions decreased to 30 per cent market share ($5.14 billion) and industrial represented 34 per cent market share ($5.81 billion).

Retail transaction volumes were down from previous years, however, declining 41 per cent year-on-year and 45 per cent lower than the 10-year average due to rising interest rates, which created a gap between buyer and seller expectations for most of last year.

Higher borrowing costs meant the retail buyer profile in 2023 was dominated by local fund managers and syndicator capital across all retail sub-sectors, which accounted for more than 40 per cent of total sales. Institutional investors sat out of retail buying last year, opting to wait until interest rates stabilise before buying assets.

“Managers have identified value in the regional and sub-regional assets during 2023, notably Haben acquiring their first regional classified shopping centre in Stockland Townsville,” Mr Willis said.

“Due to the higher cost of debt we have [also] witnessed an increased participation from ultra-high-net-worth investors, who have a lower cost of capital.”