Australia’s big shopping malls are back in black

Australia’s big shopping centres have been the quiet performers of 2024.

Despite the cost of living pressures and the challenge of online shopping, retail rents are now rising in the best centres, and, as the long-term falls in value stabilise, total returns in the malls have bettered those in the office towers or, surprisingly, in logistics.

Underpinning those shifts, for retailers and investors, is the key property factor, the lack of new supply.

Trevor Gerber, the chairman of the $9.5 billion Vicinity Centres, told his AGM last month that despite the “relatively flat retail sales growth environment” retailer confidence was robust with more than 2000 leases struck during the 2024 financial year, at generally increased rents, and on terms that “strengthen our current and future income profile”.

In the longer term, he said, “the fundamentals of Australian retail property continue to be favourable, supported by population growth, strong employment, the increasingly symbiotic relationship between physical retail stores and online, and [my italics] with limited investment in new retail supply.”

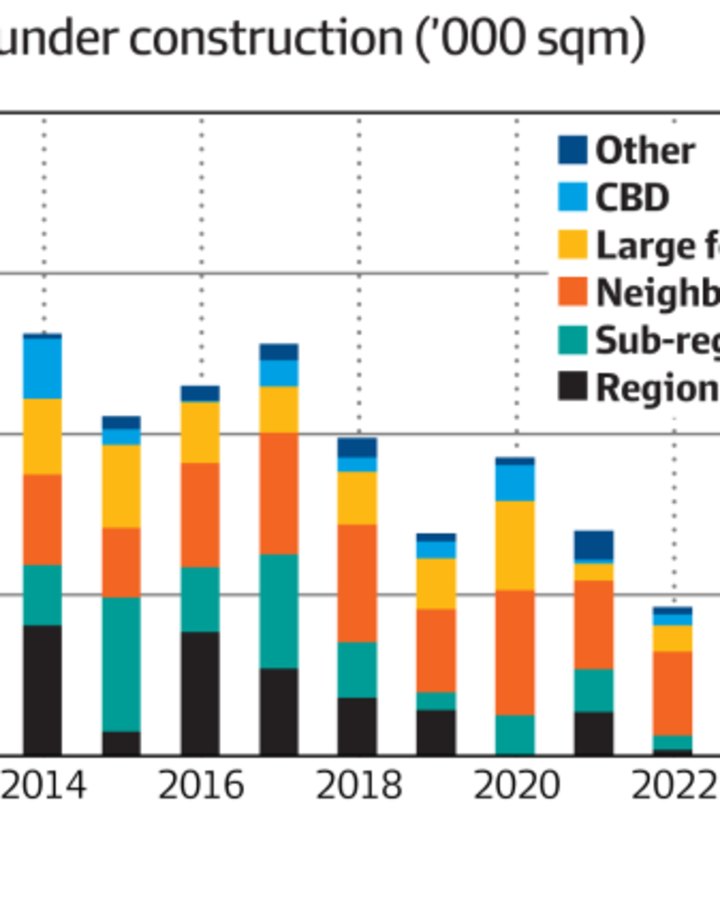

Today’s graphic, from JLL Research and Oxford Economics, underlines the point.

JLL’s head of capital markets research in Australia, Andrew Quillfeldt, says that in the four years to 2027, new retail supply will fall more than 1 million sq m short of the shopping space required by the growth in population.

More space will require higher rents. US retail property owner Kimco Realty recently pointed to the historically low new supply in US strip centre retail and estimated that in the 50 top markets across the country, retail rent would need to increase by an average 65 per cent to encourage new building.

The demand from retailers for space is surprisingly “robust” given the economic pressures and the failure of traditional tenants like Mosaic Brands.

For years real rents fell as incoming retailers paid less rent than that paid by the outgoing occupant. No longer; rental spreads are now positive.

In the September quarter, GPT group struck new leases at rents on average 3.5 per cent above the outgoing figure and usually with annual average fixed rent increases of 4.9 per cent.

For Scentre Group the average specialty rent spread was 2.7 per cent in the September quarter, coupled with annual, inflation-linked, rental rises of around 5.5 per cent.

Scentre chief executive, Elliott Rusanow, says the “demand for space, from a diverse range of business partners, is strong”.

Not from the fashion retailers who once underpinned the malls. When Scentre reworked the department store space in Westfield Mt Gravatt, the new occupants included Uniqlo, Powerhouse Gym and entertainment outlets Area 51, Holey Moley and Hijinx Hotel.

Leighton Hunziker, who as the director of retail services at Savills acts for retailers, says the big mall owners have done a good job in curating the malls with “high touch, high engagement” retailers.

Simon Fonteyn, executive director of FLNT, an online provider of leasing data on shopping centres, large-format facilities and fuel outlets, points to increased retailer interest in fast-food pads around shopping centres, to the health and wellness sector, and from luxury retailers who are bypassing traditional CBD stores and going direct to the high-class precincts of the biggest malls.

The new tenants are moving into regional shopping centres that are worth a lot less than they were a decade ago.

JLL’s Quillfeldt estimates that regional shopping centre values fell 6 per cent in the two years ahead of COVID-19 due to concerns about income sustainability, another 14 per cent during COVID-19, and then 11 per cent with the post-COVID-19 rise in bond rates. In all, that puts the rewind in values close to 30 per cent.

For some properties the fall has been far greater, much further in fact than the discounts now so much the talk of the office towers.

Half of Westfield West Lakes changed hands this year at a discount of over 35 per cent to its peak book value of a decade ago. And last year Vicinity bought back half of Sydney’s Chatswood Chase for 45 per cent of the price paid last decade.

Simon Rooney, the head of retail capital markets for CBRE Asia Pacific, says the big shopping centres now offer a “compelling value and return proposition, underpinned by robust return fundamentals and enhanced by the lack of supply and strong population growth”.

Last week MSCI announced that larger shopping centres were “back in favour”, with transactions up 53 per cent for the first nine months of the year to deliver the best year since 2018.

“Whilst grocery-anchored centres have driven retail activity in recent years, the demand has broadened to include regional, major and super-regional centres, driven by population growth and anticipated rate cuts in 2025,” said MSCI’s head of Pacific Real Estate Research, Ben Martin-Henry.

On the MSCI numbers yields on regional shopping centres have compressed for two quarters, reversing seven years of rising yields and pointing to an increase in values.

The value shift is contentious, with a big test to come when the real estate investment trusts report the year-end valuations.

Interest rates

JLL’s head of retail investments, Sam Hatcher, says that competition for prime shopping centres has “notably increased” in the past six months and likely to lead to a tightening in shopping centre yields over the remainder of 2024 and into 2025.

But UBS analyst Tom Bodor, writing after Scentre’s third-quarter update last week, argued that on the evidence of sales like Tea Tree Plaza, Joondalup and West Lakes, the cap rates on regional shopping centres are still higher than Scentre’s June 30 average of 5.4 per cent.

Which means, on Bodor’s analysis, Scentre’s valuations are still too high. UBS has a sell rating on the stock, with a price target of $3.53, arguing that the discretionary spending that fuels the big centres will deteriorate as interest rates remain higher for longer.

Nevertheless, the stabilisation of values, coupled with the increase in income, is delivering total returns for the sector ahead of those in office and logistics.

Of ISPT’s nine property funds, only one, the $2.5 billion shopping mall fund that holds smaller local shopping centres, delivered a positive return.

Similarly, in the 12 months to June 30, GPT’s $13.7 billion retail portfolio outperformed the group’s office and logistics sectors with a total return of 5.1 per cent.

Beyond the metrics of retail supply and demand lie the possibilities for other development opportunities on what are huge, well-located holdings. But that’s another column.