CEFC, $11b Goldman Sachs fund will invest in low-carbon developments

The Clean Energy Finance Corporation will co-invest with capital from a $US7 billion ($11 billion) Goldman Sachs fund to offer construction debt to Australian residential and office projects that measure their whole-lifecycle carbon footprint and disclose the efforts to mitigate those emissions.

The federal government’s green bank will co-invest $160 million alongside funds from the Real Estate Credit Partners IV (RECP IV) fund, one of a growing pool of funds investing under governance principles of the European Union’s Sustainable Finance Disclosure Regulation.

“There is greater focus on next-generation, energy-efficient buildings globally and in Australia as the drive towards sustainability continues to shape real estate demand,” said Jim Garman, global head of real estate at Goldman Sachs Alternatives.

“From our experience investing in Australian real estate we are seeing new opportunities emerge from sustainability and other secular trends.”

Critics including Clean Energy Investor Group chief executive Richie Merzian say the CEFC should not compete with private investment, but lead the way into riskier areas the private market was not yet comfortable with. However, CEFC’s investment would draw others into higher-credentialled projects with clear rules, CEFC head of property Michael Di Russo said.

“We are pushing the market further than where the current market is operating at,” Mr Di Russo told The Australian Financial Review on Tuesday.

“This opportunity is about getting a lot of those learnings that we do on a direct[-funding] basis, and putting it into a framework that other capital can come alongside and lend through.”

The CEFC is not putting money into the $US7 billion fund that closed last year, but will disburse it into projects alongside the Goldman Sachs fund under investment rules of the so-called Article 8 funds.

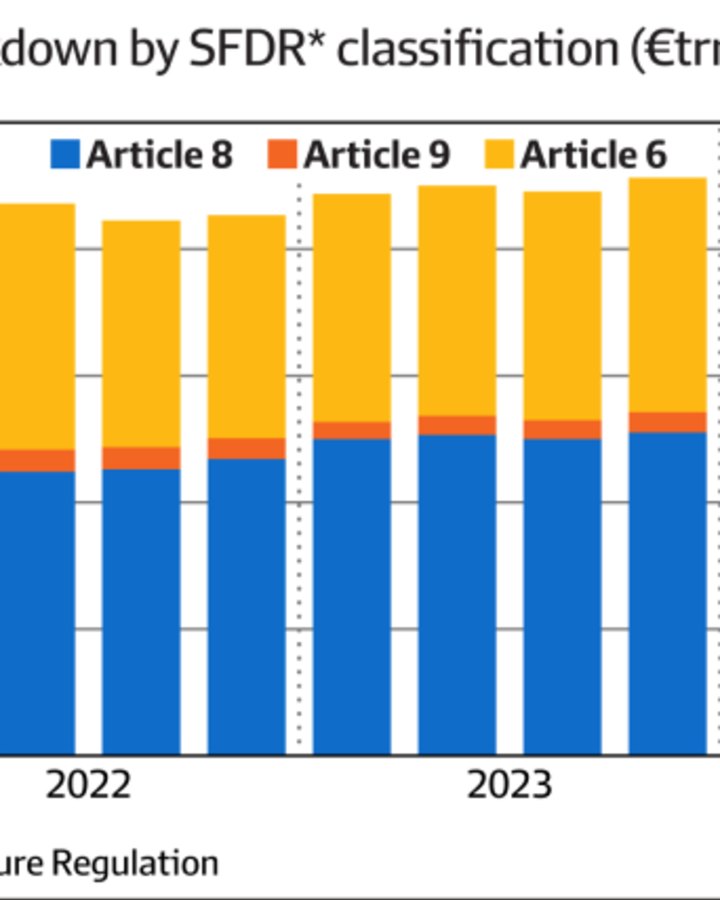

Of the three levels recognised under the EU rules, Article 8 funds must include environmental or social characteristics in the investment process.

Article 8 funds, which figures from investment research company Morningstar show accounted for nearly 60 per cent of the €10 trillion ($17.2-trillion) of funds invested under the EU principles in the December quarter, are more rigorous than Article 6 funds, which do not promote environmental, social or governance factors.

They are, however, less demanding than article 9 funds, which pursue specific sustainability objectives such as climate or social benchmarks, and which account for the smallest sliver of funds in the EU regime.

“Our understanding from reviewing the EU market was that article 9 was obviously progressively more than article 8,” Di Russo said.

“What we want to do through these other investment opportunities is progressively try and work to that basis. We want to go from reporting on prioritising sustainability to having structured documents that are actually driving absolute outcomes.”

A Morningstar report from January on the EU sustainable finance disclosure regime shows that in the last quarter of 2024, Article 8 funds netted an estimated €52 billion of net new money, boosted by inflows inot fixed-income funds.

That contrasted with an outflow from Article 9 funds, from which redemptions continued for a fifth quarter, as investors withdrew a quarterly record €7.3 billion from the funds, up from €3 billion in the September quarter.

About 40 per cent of the 50 billion tonnes of carbon emissions released globally each year come from the built environment, and 22 per cent comes from embodied carbon emissions in infrastructure and construction, figures KPMG published in 2023 show.

Projects funded under the co-investment program will have to show minimum standards across operational energy efficiency – through measures such as electrification and use of renewable energy – and embodied carbon, while additional requirements include the preparation of physical climate risk assessments, the CEFC said.