Understanding the property cycle can be very useful for commercial real estate investors to help them decide on their next move – be it to buy, build or sell.

There are four phases to the commercial property cycle and each offers different opportunities.

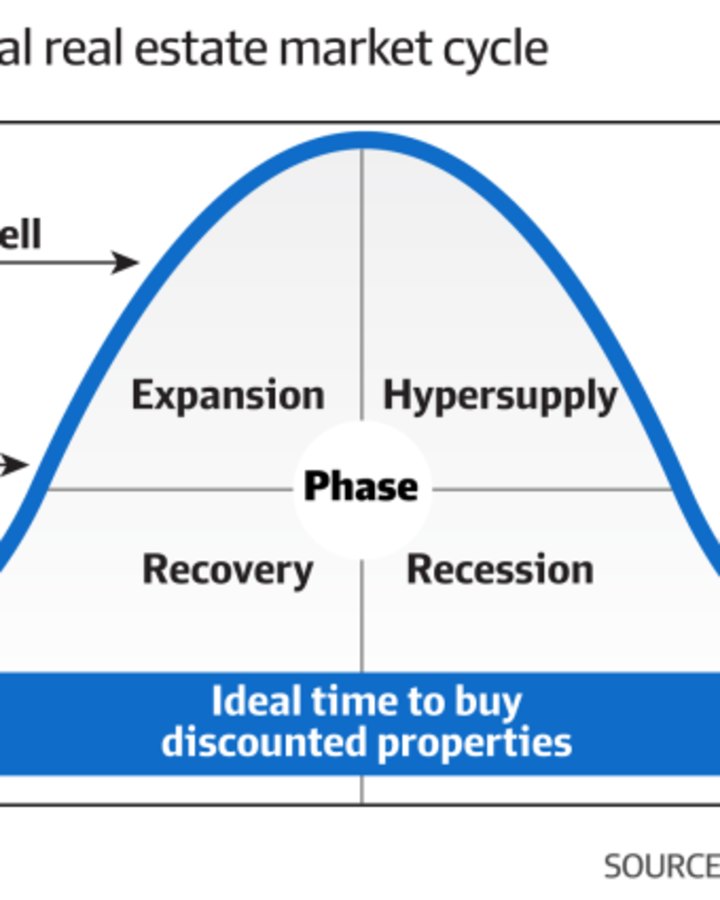

The first is recovery, when property starts moving up from the bottom of the trough. Excess construction activity from the previous peak of the cycle has stopped, and new construction is limited. Occupancy rates are low and rental growth might be flat or declining. In the broader economy, interest rates are low, jobs growth is picking up and confidence is improving.

This can often be a good time to pick up properties at a steep discount.

Phase two is expansion, when demand increases and vacancy rates drop. Construction activity is also picking up and there is more competition for commercial real estate assets, with a resulting increase in prices. We see rising interest rates, robust economic growth and continued jobs growth. This phase can present opportunities to start a development or upgrade as the market rises.

The next is hyper-supply, when too much construction activity starts to create an oversupply of properties and prices start to decline.

Interest rates continue to rise, jobs growth stalls or declines and the economy slows. Property owners looking to sell would do well to divest before the next and final phase.

In the fourth phase – recession, buyers are thin on the ground and property prices can suffer steep falls. In the broader economy, unemployment is rising and confidence is deteriorating.

This can also be a good time to purchase property, although there’s always the risk that the phase lasts longer than the investor budgets for.

Office property still in recession

Looking at the four stages makes property investing seem easy: buy at the end of the recession phase and sell in the expansion phase. What could be simpler?

That’s the theory, but it’s not always as easy in practice. Usually, the various indicators will point in different directions, and it’s only with the hindsight of a few months or even years that we can pinpoint exactly where we were in the property cycle.

Additionally, the recession phase and the recovery phase look quite similar.

With these warnings in mind, it is nonetheless worth trying to establish where we are in the cycle for commercial property asset classes. For office property, the answer is that it is still in the recessionary phase.

Big office landlords are selling assets and carrying out significant write-downs of the properties they’re holding on to. The write-down of office funds accelerated over the April to June period to minus 8.7 per cent, double the losses for the first three months of this year, according to MSCI data.

More write-downs of office properties are anticipated as inflation, higher interest rates and geopolitical risks weigh on capital flows and market sentiment.

On the face of it, this might look like a good time to buy, but investors need to be careful that they’re not catching a falling knife. The office sector is a longer-term play than some other asset classes and they should be confident in their plan to turn an asset around.

Retail looks as if it’s further along in the property cycle – moving into the recovery phase. This market has been a lot more active than the office market and two big deals in Western Australia last month have boosted confidence that retail property is recovering.

Queensland Investment Corporation sold its interest in Perth mall Claremont Quarter for $207 million, which QIC’s real estate capital markets director, James Doneley, said was above book value.

And ASX-listed shopping centre operator Vicinity bought a half-stake in Lakeside Joondalup for $420 million and said it had lifted occupancy to levels last seen before the pandemic.

Industrial property is less clear-cut and depends on the market. In Sydney, the market looks like it’s still in the expansionary phase. Rents are growing strongly and supply is constrained because of a lack of development opportunities.

Rents in Melbourne have also been rising, but there’s more space for new supply to come on, so it looks as if we might head into hyper-supply in the Victorian capital. That said, it could take time because some unmet demand appears to be spilling over to Melbourne, in particular from Sydney, as companies shift their logistics operations south.

Of course, we’ll know exactly where we are in the cycle for each of these asset classes only in a year or two when we’ve seen prices rise or fall. Even so, it’s useful to have a view of where the cycle is up to before making any decisions.

The acquisition of the Bell family’s Australian Food & Agriculture Company for $780 million includes 95,000 merino sheep.