‘Pay to stay’: Average Sydney hotel room rate to hit $426 by 2033

Sydney will surge further ahead of all other capital cities as the country’s priciest hotel market over the next decade, as rising demand for accommodation in Australia’s biggest city outstrips only a moderate increase in new supply.

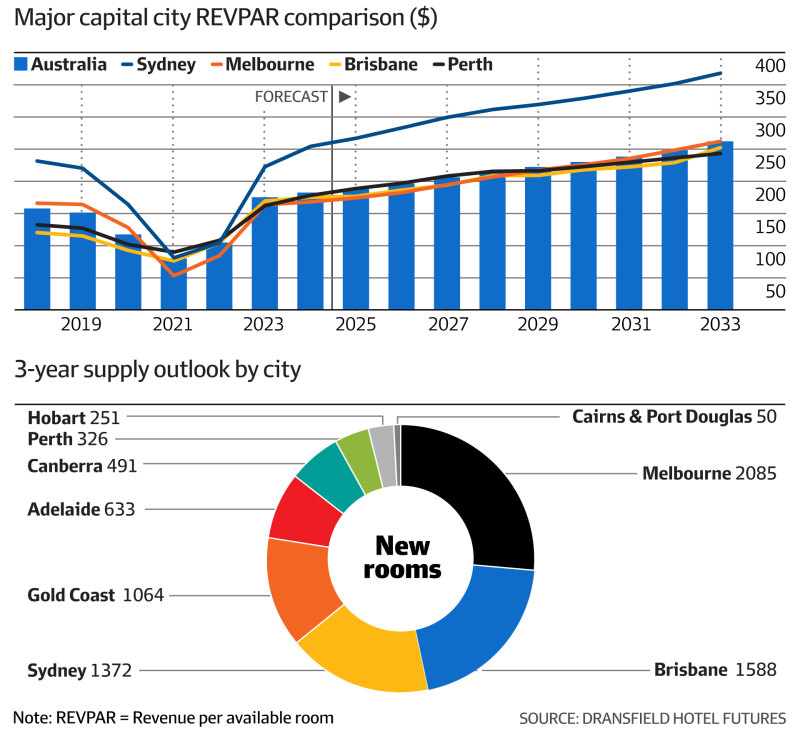

By 2027, the average price for a night’s stay in a Sydney hotel will hit almost $350 and then reach $426 by 2033, according to the Hotel Futures 2025 report by analysts Dransfield.

With occupancy to peak at 86.4 per cent by 2033, Dransfield said Sydney was “returning to the past” – referring to the very strong pre-COVID operating period for hotels – and was “expected to again be effectively ‘full’ within the next two to three years”.

This strong outlook follows Sydney ranking as the top-performing capital city over FY24, as it delivered 14 per cent growth in revenue per available room (revPAR) of $254. RevPAR is the key industry performance metric calculated by multiplying occupancy by average room rate.

Sydney was the only capital city to record an 80 per cent occupancy rate over FY24 while its average room rate rose 3.8 per cent to $317.

“Sydney is the standout performer, with its absolute [revPAR] position more than $100 higher than any other city at the end of the forecast period. The continued lack of material supply in this gateway city drives very high occupancy,” the Dransfield report noted.

“We expect the elevated post-COVID room rates will persist in these [supply constrained] conditions, with the market coming to accept that you will need to pay up to stay in Sydney.”

Next best performer – on a revPAR growth basis – was Perth (10 per cent growth to $190) followed by Cairns and Port Douglas (4.1 per cent to $158), Brisbane (3.4 per cent to $175) and Melbourne (2.5 per cent to $168).

Looking at future supply, Sydney is set to add just under 1400 new hotel rooms over the next three years – an increase of just over 5 per cent – compared with a 10 per cent increase between 2019 and 2024, a period in which a number of projects that were delayed by the pandemic were completed including W Sydney at Darling Harbour.

The Dransfield report notes that Sydney is expected to remain “supply constrained over the long term” with “site availability and highest and best-use contests the primary impediments to supply growth”.

“At the simplest level, well-located residential is still selling for up to three times the [per] square metre rate of hotels,” the report said.

Melbourne will add just over 2000 rooms (6.6 per cent growth) over the next three years (a marked downturn from the near 5000 new rooms delivered between 2019 and 2024) with Brisbane growing by 10.2 per cent or almost 1600 rooms as it bumps up accommodation capacity for the 2032 Olympics.

Hotel mogul Jerry Schwartz, whose family owns properties like the five-star Sofitel Sydney Darling Harbour as well as more affordable offerings like the Mercure Sydney and ibis Sydney World Square said his three and four-star hotels were the strongest performers in his portfolio.

“These hotels are performing really well. Last month our Rydges Sydney Central had a 94 per cent occupancy rate,” Dr Schwartz told The Australian Financial Review.

But he said room rates were down about 10 per cent at his flagship Sofitel Sydney Darling Harbour due to lower occupancy levels, something he attributed to the cost-of-living crisis.

“People are choosing cheaper holidays. The opposite occurred during COVID, when everyone splurged a little bit and paid a bit more to stay in a nice hotel,” he said.

Dr Schwartz said it was really good to hear that new development of hotels was being restrained, as this would push Sydney back to being full.

Paul Salter, managing director of Salter Brothers, which owns and operates 41 hotels including Sydney’s Crowne Plaza Coogee, the Intercontinental Rialto in Melbourne and voco Gold Coast, said the fund manager was “very positive” on the Sydney market where demand is outpacing supply.

“The opening of the new international airport in Western Sydney in 2026 should mean Sydney generally is stronger,” he said.

“The Gold Coast and Melbourne are good, but not great markets. Melbourne is absorbing a lot of supply, which is what Melbourne does. On the Gold Coast the leisure spend is strong.”

Mr Salter said its luxury hotels were performing pretty well as were its suburban hotels and regional resorts driven by the “road warrior market”.

Overall, the outlook for the hotel sector is buoyant on the back of strong growth in domestic and international tourism and increasingly busier events and conference calendars, supported by lower interest rates, according to Dransfield.

The advisory firm is forecasting average annual demand growth of 3.3 per cent to fiscal 2033, but only 2.2 per cent annual supply growth over the same period as new projects are driven by “market responses” (actual need for new hotel rooms) compared with a more speculative approach before the pandemic.

In Melbourne, which has absorbed more new hotel stock than other markets, Dransfield said there were several years in its recovery arc before occupancy levels reach 80 per cent and rates can start climbing. Brisbane is expected to reach an 82 per cent occupancy rate by 2033, according to Dransfield.

Among the emerging development trends, Dransfield said were a “general shift to quality” as the cost of land and construction making entry-level products in core CBD locations less feasible.

Hotels are also set to get smaller as guests look for a “more tailored and authentic experience, and the availability of land reduces”.

“Hotel developments in excess of 250 rooms is reducing,” the report notes.

Dransfield said hotel operators were focusing more on their food and beverage offering and seeing less value in buffets and “basic dinner offerings”.

“A destination restaurant or bar is now considered a way to help position the whole hotel and drive both room and F&B revenue advantages,” Dransfield said.