Prospects brighten for property stocks as 2024 rate cuts loom

The prospect of interest rate cuts in 2024 has significantly buoyed the prospects of listed real estate companies, whose fortunes are closely tied to the cost of debt.

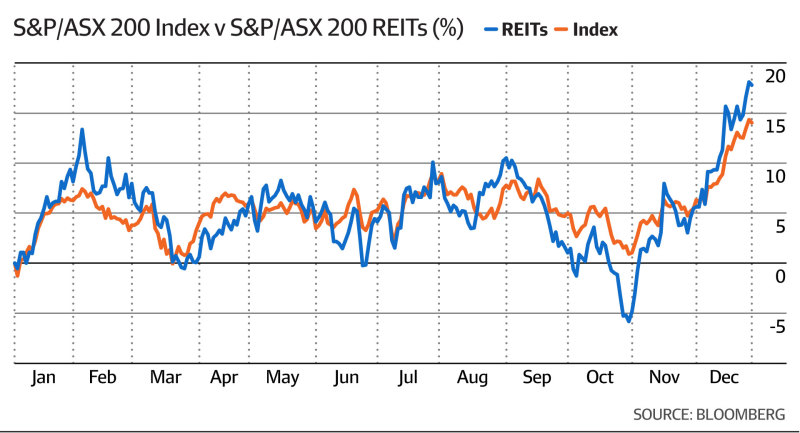

In the final months of 2023, the real estate investment trusts (REITs) took off as inflation eased globally. The sector delivered almost 12 per cent over the year, with the bulk of the gains achieved in the past three months, outperforming broader equities which closed a little above 8 per cent for the year.

Driving the REITs’ rebound was the sharp fall in bond yields – which move in the opposite direction to bond prices – as traders readjusted their expectations on the rate cycle. Yields on 10-year Australian Treasury notes fell from near 5 per cent in October to below 4 per cent by the end of 2023. REITs are typically viewed as bond proxies, whose valuations can pick up as Treasury yields dip.

“The outperformance of the sector in 2023 was largely driven by the expectation for lower bond yields and rates in the last quarter of the year,” Jarden analyst Lou Pirenc and his colleagues wrote in a client note just before the Christmas break.

“One’s view on rates is not only critical to whether this outperformance can continue but also for how to position within the sector.”

While hopes are rising globally that central banks will begin cutting rates some time this year, the Jarden view is based on no cuts until 2025. So, while stable rates would still be positive for the REIT sector, they would also maintain the pressure on earnings and asset values, Mr Pirenc noted.

“In our base case, we believe stocks with stronger balance sheets and superior earnings momentum will outperform.

“If we are wrong on rates and the RBA cuts happen earlier, residential developers – Mirvac, Stockland – should be key beneficiaries.”

Other “deep value” stocks, especially those with funds management operations such as Charter Hall, Centuria, GPT and Dexus would also benefit if borrowing costs fall and the sluggish transactions market – which has been stalled by the wide bid-ask spread – cranks back up. Global logistics giant Goodman has posted gains well above 40 per cent in the past year, but could be a relative underperformer if rates are cut earlier than Jarden expects.

Were it not for the stellar performance by Goodman, the REIT sector would be trailing the broader equities performance, UBS analyst Grant McCasker and his colleagues have written in a recent client briefing.

But that also means that if Goodman were excluded, then, in a rate-cutting cycle, the REIT sector “moves up the pecking order within Australian equities, no longer warranting the perennial underweight allocation”, Mr McCasker wrote. UBS has a “buy” rating for Goodman, courtesy of its sustainable earnings growth and its increasing interest in data centres.

As the headwinds of debt costs ease – UBS expects material cuts to rates in 2024 and 2025 – the likelihood of earnings upgrades increases, after two years of downgrades.

Another boost for the REITs sector in 2024 comes from the fact that the market has already priced in expected devaluations of their commercial property portfolios – totalling around 18 per cent for office and mall assets.

Investors are already looking past any more asset writedowns – which are expected to bottom this year – and so now expect a positive performance in the listed market, according to UBS.