Tough times for orchards, vines send values plummeting

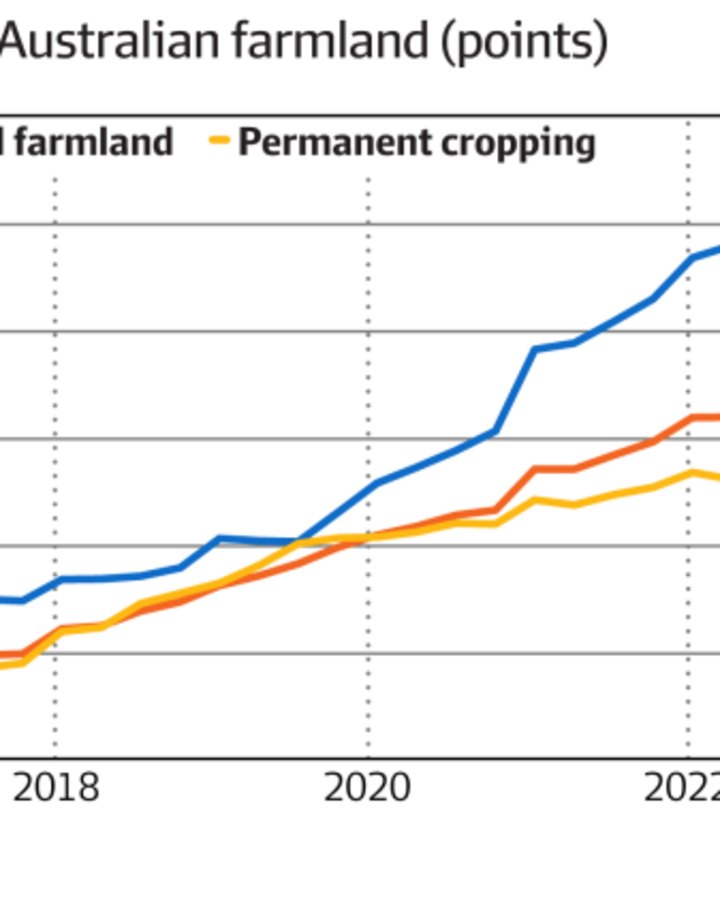

Capital values for orchards and vineyards plunged more than 18 per cent in the 2024 calendar year, the result of poor commodity prices and higher costs for some crops, according to the ANREV Farmland Index.

The poor returns from permanent farmland including horticulture delivered income growth of just 0.78 per cent annualised and sent total returns for all forms of farmland to negative 3.81 per cent for the past year.

In sharp contrast, annual farmland prospered. Capital growth and income rose substantially in that category, which takes in land used to graze livestock or grow annual crops such as wheat and barley. It was buoyed in particular by strong demand for Australian beef in the US and South-East Asia.

By the December quarter, capital growth for annual farmland was up 6.1 per cent over the previous 12 months, according to ANREV. Income had grown 2.89 per cent, taking total returns to 9.14 per cent.

The ANREV index tracks the performance of 63 properties worth $2.2 billion, managed by major agricultural asset managers such as Gunn Agri Partners, Manulife Investment Management, Growth Farms Australia and Rural Funds Management.

ASX-listed Rural Funds Management, which has exposure to orchards and vineyards as well as broadacre farms, noted the country’s livestock industry last year exported its largest ever volume. The strongest growth for beef exports was to the US, up 60 per cent, and South-East Asia, where exports lifted 33 per cent.

Lamb production was up as well, while cotton production was forecast to be well above the 10-year average, it said.

Grape oversupply

Meanwhile, the big drop in capital returns last year for farmland planted to permanent crops was largely driven by citrus orchards, where prices for navels and mandarins are under pressure.

Other permanent farmland areas with multiple crop types – wine grapes, grapes and stone fruits – also suffered in the December quarter as input costs rose to prepare for harvest. Those costs are expected to be offset over subsequent quarters as crop revenue is recognised.

As well, warm-climate grapes have been hit because of a large oversupply.

“Market conditions for citrus and other summer fruits have improved substantially, with exports pushing new levels and higher domestic and export prices,” Rural Funds said.

“An exception being table-grapes, which have not been as fortunate, experiencing a poor production season.”

Separate figures on farmland prices released by the Australian Bureau of Agricultural and Resource Economics in the past week paint a wider picture beyond corporate agriculture. They show broadacre farmland prices have effectively levelled off in the past two years after a decade of strong growth that pushed rates higher by more than 10 per cent annually on average.

“Instead of using the war chest they’d built in good seasons to look for investment, [producers] looked to use it for working capital.”

Dr Jared Greenville, ABARES executive directors

The trigger for that levelling off came as the terms of trade tightened for Australian producers, ABARES executive director Dr Jared Greenville told The Australian Financial Review.

“We went from a perfect storm of excellent seasonal conditions and really high global prices. Land prices jumped and we had more money in the system with people making investments,” he said.

But as inflation rose, the supply chain was squeezed and farmers faced higher costs for imports, domestic prices for sheep and beef fell and those producers chalked up losses.

“So instead of using the war chest they’d built in good seasons to look for investment, [producers] looked to use it for working capital,” Greenville said.

The impact of those changing fortunes is apparent in the lower volume of broadacre farmland transactions, which decreased from 4445 transactions in 2021 to 2258 transactions in 2024, according to the ABARES Farmland Price Indicator.

However, the outlook for broadacre producers – and farmland prices – is rebounding, according to Greenville, with parts of the country, especially in Western Australia, looking profitable.

“This [financial] year 2024/25 we are expecting the average broadacre farm cash income to go up by around 70 per cent, and similarly for profits,” he said.

“Part of that is the easing of inflation, easing of cost pressures and a return to better livestock prices in particular and improved production outside of South Australia,” Greenville said, noting as well the jump in livestock prices and higher volume of export into the US.

“As it has in the past, we would expect this would be supportive of farmland prices,” he said.

However, Greenville noted that still to be factored into that rosier outlook was the uncertainty over potential fallout for Australian farmers, especially beef exporters, from US President Donald Trump’s tariff war.