Why commercial property is at a turning point

The outlook for commercial property is brightening, with real estate investment trusts around the world reporting improved operating income and, with more willing buyers, a trough in valuations.

At the same time, supply is constrained, and interest rates have peaked.

For many, that’s a turning point. Even the start of a new cycle. But as always in property, the turn will take time, and will play out differentially across sectors and markets.

Charter Hall managing director David Harrison told analysts that income is always the first to recover, and valuations follow, but stressed that the “best growth is enjoyed in the early part of the cycle”.

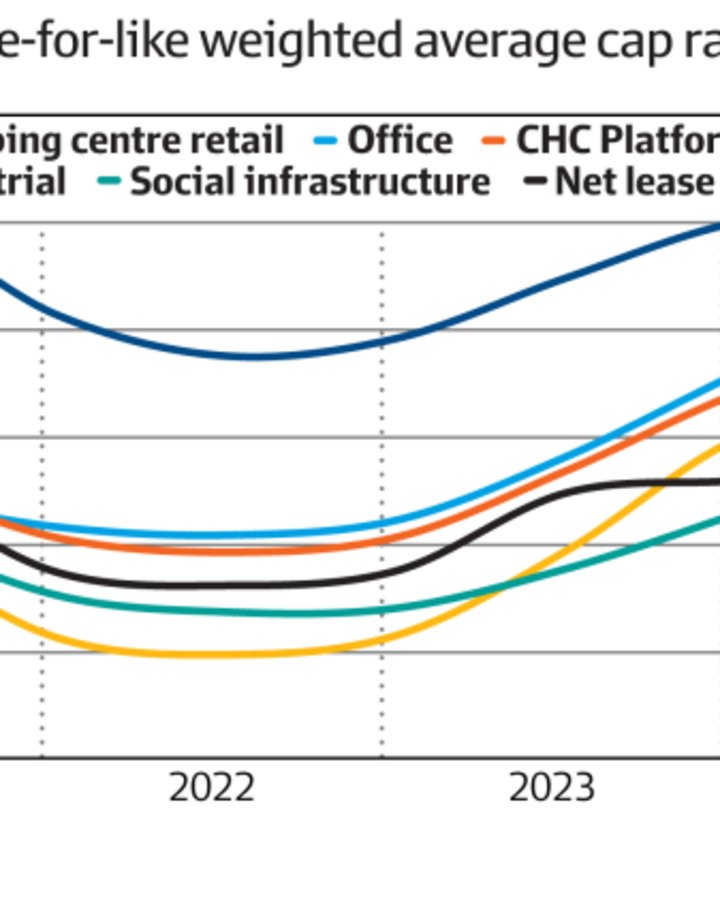

The valuations across the Charter Hall funds – reported in the parent stock’s results pack – reflect what has happened across the broader market in the December half.

A small increase in cap rate – equivalent to a small decline in value – has been largely offset by an increase in income.

Effectively valuations troughed during the half before rising a tad, by an average 0.8 per cent for industrial and logistics property and 1.2 per cent for shopping centre retail.

Office woes continue

Only the office sector has seen a further fall in valuations. But even that decline, 3.5 per cent, is marginal compared to earlier periods.

And Harrison argues that cap rate decompression is now “overdone, particularly for good quality assets”.

The accompanying graphic from Charter Hall shows that yields across the group’s funds have largely retraced their post-COVID tightening.

And because of underlying rental growth, the actual values are well up on their June 2020 numbers – by 35 per cent for industrial and 19 per cent for shopping centre retail.

The exception is office, where values are still 5 per cent below 2020 figures.

The office sector continues to lag, despite the more positive commentary from industry leaders, and more talk of the return to office.

GPT chief executive Russell Proutt highlighted the “significant lift” in his group’s office occupancy, to 94 per cent, but with the average incentive for the year at 35 per cent the group suffered a 2.9 per cent decline in office portfolio income and a negative 5.6 per cent return for the December half.

GPT, like its peers, enjoyed a better return from its industrial and logistics portfolio, although most observers argue the extraordinary post-pandemic rental growth is coming to an end.

Rents still rising

Big uplifts in rent are still being experienced, with GPT enjoying leasing spreads of 35 per cent in its logistics portfolio over the year and “further income upside” is expected from a portfolio that is still 15 per cent under-rented.

The Centuria Industrial REIT, the only REIT exclusively focused on local industrial property, enjoyed a spread of 50 per cent on the leases negotiated in the December half.

Of course, over time that releasing spread will narrow, as the leases struck before the COVID-19 rental surge are renegotiated and the growth normalises.

Centuria Industrial REIT manager Grant Nichols also noted a “bifurcation” between urban infill locations, where the vacancy is 1.8 per cent and rents rose 8.9 per cent during the year, and the outer-fringe locations where the vacancy is 3.3 per cent and the rental growth a softer 4 per cent.

For GPT the best performance for the year came from shopping centres, where both income and valuation increased in a pattern reflected across the sector, and underpinned, as Vicinity Centres noted, by the fall in retail space per person across the country.

On Wednesday Westfield’s owner and manager, Scentre Group, reported its fourth year of income growth, enough to overcome increased spending on security, and, as the downturn in valuations came to an end, enough to deliver a statutory profit of over $1 billion.

The guidance for 2025 disappointed investors, but the logic for the broader market is clear. Available space is scarce, in fact non-existent in 19 Westfield centres, while post-pandemic demand is growing and leasing spreads, which for many years were negative, are now solidly positive.

Managers of real estate funds

The other sector that shone through the results was managers of real estate funds – Charter Hall Group and HMC Capital – which delivered good results and solid outlooks.

UBS analyst Tom Bodor, said the outlook for the managers reflected new equity flows and, as liquidity returns to the sector, the ability to raise more capital.

Andrew Parsons, the chief investment officer of global listed real assets manager Resolution Capital, said if bifurcation was the word for 2024, “inflection is the word for 2025”.

“Values and operating conditions seem to be turning the corner in several markets and sectors,” he said.

Parsons had two cautions. The benign economic growth picture, which underlines that the turn may become more tempered. And interest rates are not returning to the lows reached in the past decade.

Amy Pham, the portfolio manager of the Pengana High Conviction Property Securities Fund highlighted the inflection point in her pre-results commentary.

Rising debt costs over the past two years have largely wiped out earnings growth but as cash rates come down, “we anticipate a return to positive sector earnings growth this year, and acceleration over the next two years as debt costs begin to ease”.

Pendal Group’s head of listed property, Peter Davidson, said he expected the sector to show earnings growth of around 4 per cent this year, excluding Goodman Group, and 8 per cent, including Goodman.

“The better growth in the vanilla – non-Goodman – listed property trusts reflects the better top line rental growth and an easing in interest rate headwinds,” he said.

Data centres, of course, delivered the excitement during the results with the $4 billion Goodman Group raising, the largest in the real estate sector, the CDC Data Centres share sale, along with comments about power capacity across the sector from the local Stockland, to global heavyweights Prologis and Segro.

Charter Hall managing director, David Harrison, whose group controls 2000 hectares of industrial and logistics land, said his funds could take advantage of “some of the hype” and play the data centre thematic “in a different way”.

Parsons said while data centres are the focus of excitement, the star sector in the US is healthcare, and senior housing in particular, with stocks such as Welltower and Ventas showing double-digit rental growth in 2024, and expected to deliver the same this year, due to demographics and low supply.

Two other features of the reporting commentary sand out.

Victoria is regularly noted as the weakest market.

And the big end of town has not lost focus on sustainability despite the negativity emanating from Washington. It is, after all, what occupiers and investors want.

Robert Harley is a former property editor at The Australian Financial Review. He can be contacted at rob@rharley.com.au